Anexo PLC Special Situation Case Study

When Insiders Offer A or B, I Choose C

This article is intended as a case study in special situations and minority shareholder tactics, it is not longer actionable as the shares have been delisted.

I will dissect the recent actions by Anexo Group Plc (ANX) insiders to take the company private. I argue that the structure of their Takeover Offer contains a critical legal vulnerability—the Achilles Heel—that presents a compelling angle for studying shareholder protection.

I. The Setup: A Deeply Discounted Target

Anexo operates through two distinct segments: Credit Hire and Legal Services. Despite significant growth since its 2018 IPO, the stock has historically underperformed for shareholders.

The business has been described in many other places, so I will limit myself to two metrics that are sufficient for understanding the following argument.

5-Year Average EPS: 13p.

Tangible Book Value (12/2024): 1.42 GBP per share.

Following recent events, the shares recently became available in the 30p range.

II. The Insider’s Gambit: Coercion and the Exit Scenario

The Joint Bidders—comprised of insiders Alan Sellers, Samantha Moss, and DBAY (a PE firm)—sought to maximize their own value by acquiring the minority stake cheaply.

Crucially, the outcome of this process involves the delisting of Anexo. Given the involvement of DBAY, a private equity firm that requires an exit, I believe the Bidders are effectively structuring a cheap entry for a future, more lucrative exit scenario, suggesting the company will ultimately be sold within a reasonable timeframe.

The Bidders Plan A intended a debt-funded take-private. However, this failed because lenders required a 75% minimum acceptance condition to secure the assets, as laid out in the Offer Document.

I point this out, because I see it as evidence that their ultimate goal and psychological anchor is a take-under at a cheap price rather than a complete destruction of minority shareholder value (as has been argued by some during the negative sentiment in prior months).

After Plan A failed, Plan B was developed. The Bidders started a Tender Offer below market value at 60p, followed by a Takeover Offer with what looked like two options:

PIK Loan Notes: Face value of 60p with a 15% interest rate. These were restricted, having a maximum duration of five years and being not transferable.

Midco Shares (Alternative Offer): This maintained economic exposure but carried the explicit threat of dilution.

By stacking detestable options, the merely bad option looks better. Hence, shareholders overwhelmingly tendered at 60p, allowing insiders to extend their shareholding and securing the success of the takeover offer.

Along with the reputation of the responsible insiders, the share price collapsed down to the 30p region as trust disappeared and appetite for Loan Notes and the Alternative Offer was low.

III. The Achilles Heel: The Legal Chink in the Armor, Option C

Reading through the materials and several news releases I found it suspicious that the Bidders portrayed only the two options A/B described above, and repeatedly urged shareholders to accept either of the options.

In fact, one could retain the original Anexo shares, although the threat of compulsory acquisition (=squeeze out of the equity and into the loan notes) was spelled out in the offer document. It was always likely that they would cross the required 90% mark, so the perfect impression was created that shareholders should just directly accept the loan notes.

However, to me this looks as if it may be the Achilles Heel of the Bidder’s case. Shareholder Protections under a squeeze out follow different rules than shareholder protections under a Take Over offer. Whereas during the latter the focus is procedural, the prior contains a focus on a fair price as stated in Section 986 of the 2006 Companies Act.

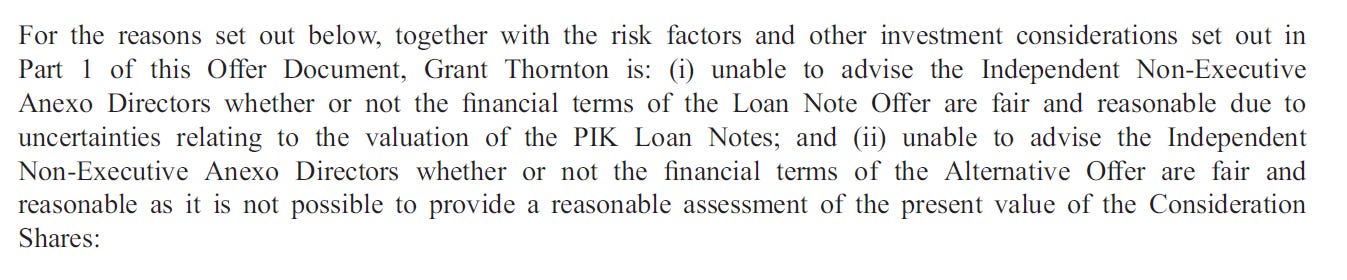

This allows shareholders to challenge the transaction in court. It is widely known that shareholders experience difficulties in judges recognizing equity value, yet I argue this case is different. While a quick look at tangible book value and EPS identifies the undervaluation provided by the takeover offer, we can just rely on Anexo’s own advisor Grant Thornton, who was not able to advise whether the Loan Notes are fair and reasonable (as per the Offer Document).

I argue that a court challenge following a possible squeeze-out would be a serious threat to the Anexo Bidders. Given that they have secured 93.3% of the shares and equity value already (as of 9 Sept) I assume a good probability that they will refrain from squeezing-out and pay a price closer to fair value to remaining minorities once they exit themselves.

IV. Conclusion: My Case Study Thesis

Following the Bidders’ Takeover announcement, the Anexo share price collapsed as negative sentiment took hold and shareholders began questioning whether the Loan Notes would be honored. I remain quite confident that if the Bidders wish to retain the value of their equity, they will ultimately need to redeem the Loan Notes as a contractual debt instrument. Given a face value of 60p and 15% annual interest, I viewed the notes as attractive when buying in the 30p range.

However, my primary conviction lies in the Anexo equity itself. Because I see higher value in the shares—and anticipate receiving the Loan Notes anyway in the event of a successful squeeze-out—I retained the original Anexo shares where possible (one of my brokers forced me into giving them up). I am curious how this will play out and remain cautiously optimistic that the Anexo equity holds more value than the debt instrument being offered.

This article contains contributions from my friend Tobias Buchwald. Connect with him here:

https://bsky.app/profile/tobi-preisundwert.bsky.social

https://www.linkedin.com/in/tobias-buchwald-91551b251/

The analysis is original - the delivery polished by AI.